Zoom: All Eyes On Up-Market

Q1 25 Earnings Review Digest

1.0 Big Customers, Big Contracts

$ZM keeps expanding among its installed base, driven by cost efficiencies realised by consolidating their communications and collaboration solutions on to Zoom, as well as a more seamless user experience.

Despite slighly beating revenue consensus, the most important metric from Q1 2025 Earnings Presentation was the following (more on this below):

The continuous rise year-over-year in the number of customers contributing >$100k in TTM (Trailing Twelve Months) revenue is the result of a maturing product offering in the up-market customers segment.

Despite the slowdown depicted in the graph below, Zoom still has plenty of room to up-sell those customers and expand among its existing customer base. In such graph, a customer contributing $200k in TTM revenue is represented in the same way as a customer contributing $101k for the same time period, although the relevance of these two customers would be quite different.

The effects that arise from customers contributing >$100k in TTM revenue would manifest themselves on the enterprise revenue growth rate (see graph below). During Q1 2025, Zoom managed to stop the downward revenue growth trend for enterprise customers and hopefully will be able to revert it towards the second half of this year as new/immature products further penetrate the market.

Products that are candidates to drive growth reacceleration include Contact Center (more on this below), Revenue Accelerator and Workvivo, which is exhibiting storng momentum, as per management.

2.0 Product Strategy

Zoom Contact Center, launched only two years ago, is ready for prime time.

- Eric S. Yuan, Zoom Founder, President, Chairman and CEO during the Q1 2025 earnings call.

As I mentioned during my original deepdive, Zoom’s core value creation mechanism is its ability to turn minimum viable products into world-class products in a short period of time.

This product development, exhibited first with Zoom Phone, can now be seen in Contact Center Solution. During Q1 2025 earnings call, management shared that Zoom had beaten a Gartner top 4 CCaaS (Contact Center as a Solution) player in a significant deal. This should not come as a surprise, given that recently more than a thousand features per quarter were being added to Contact Center, creating a very compelling case for customers

The early success of Contact Center has led to the milestone of reaching 90 Contact Center accounts with >$100k ARR (Annual Recurring Revenue), indicating a 246% increase year-over-year.

Additionally, Zoom also amassed five Zoom Phone customers with >100k seats.

Since the introduction of different pricing tiers for Contact Center, ASP (Average Selling Price) has almost doubled quarter-over-quarter. As additional features and functionalities are added, pricing for those and upper tiers will also increase. This is expected to turn into margin expansion.

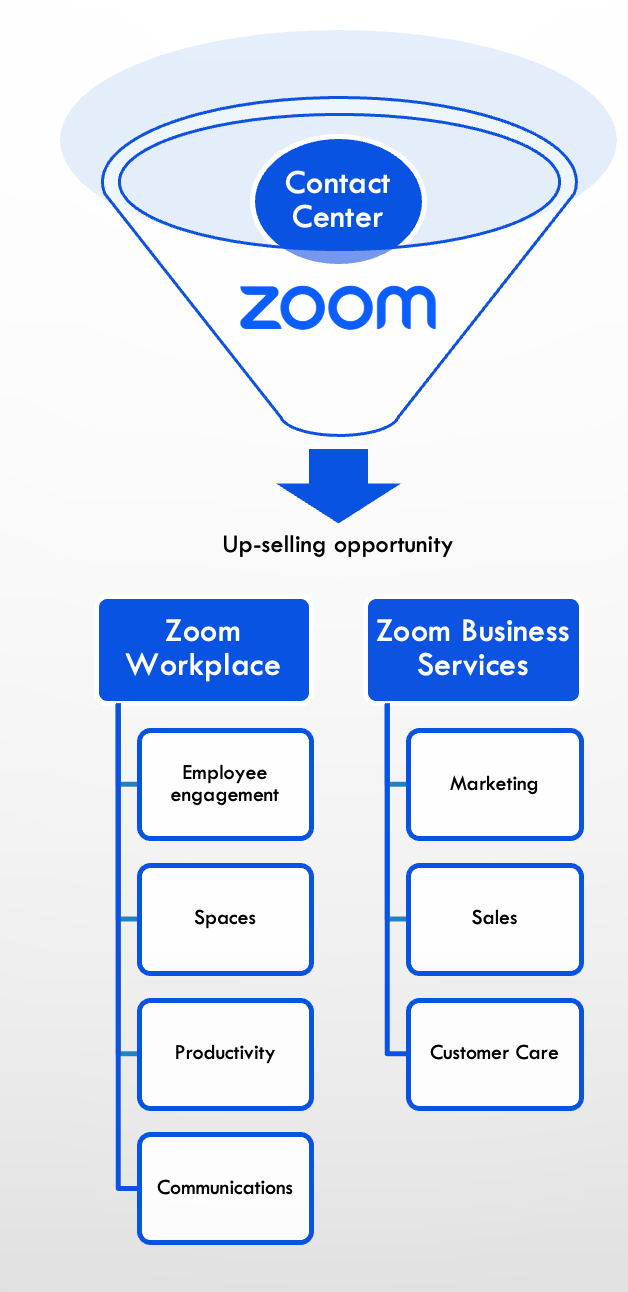

As Eric mentioned above, the launch of Contact Center is bringing new logos to the company, enabling opportunities within the wider Zoom ecosystem and channeling customers to Zoom Workplace and/or Zoom Business Services at marginal cost:

Eric also shared during the call that AI Companion will be leveraged to build new products and services such as Ask AI, which will be introduced later this year.

3.0 International Expansion

In the previous quarters, ROW (Rest Of the World) revenue was impacted by the (delayed) reorganisation of the international sales team. With this now complete, Zoom should have a clear path to resume international growth.

America continues to be Zoom’s engine growth, growing 4% YoY, which is significantly below the growth rate achieved during Q1 2024. However, EMEA (Europe, Middle East and Africa) has returned to growth (2%), and APAC (Asia Pacific) continues to be impacted by FX (Foreign Exchange) headwinds (-2%).

4.0 Zoom’s Growing Cash Pile

$7.4bn cash pile, or 38% of market cap.

FCF (Free Cash Flow) for Q1 2025 soared to $570m, up 44% year-over-year, driven by higher cash from operating activities ($588m vs $418m during Q1 2024).

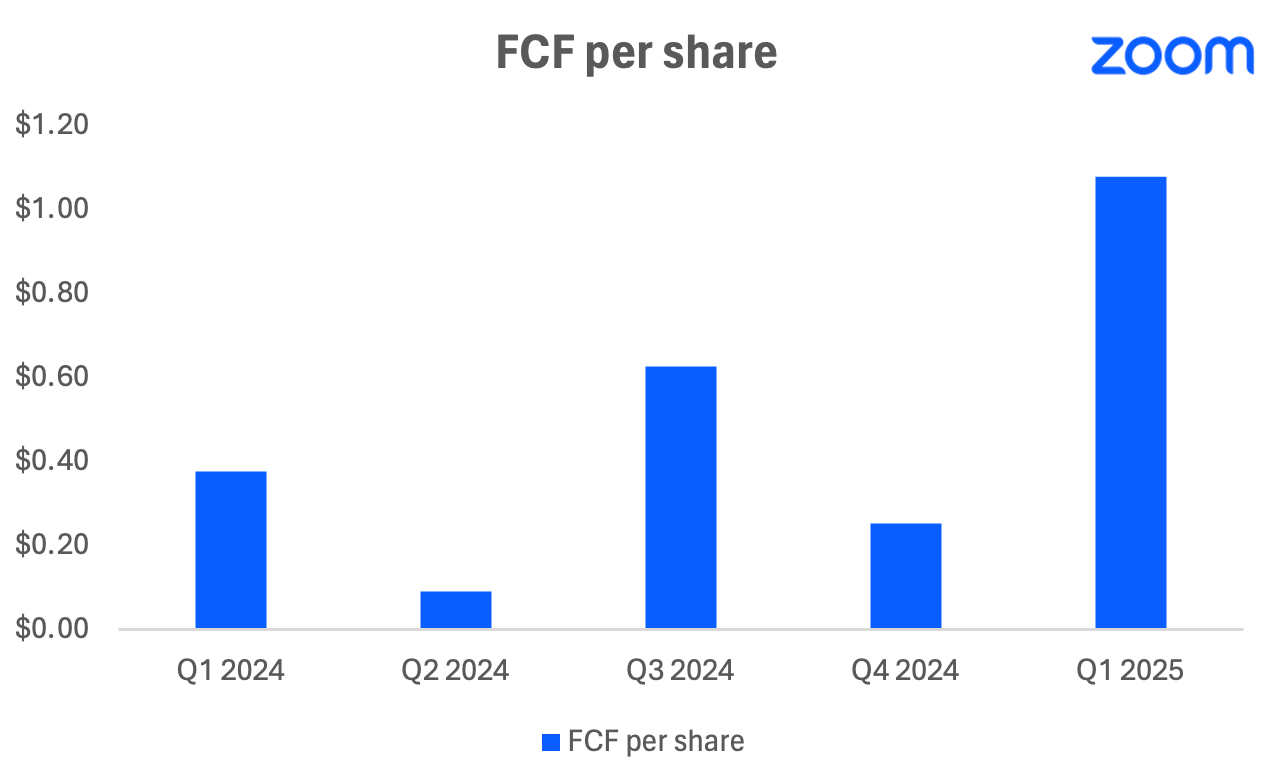

Free Cash Flow per share for the quarter (calculated as (Cash From Operations - Purchases of PPE - Stock Based Compensation Expense) / Diluted Weighted Average Shares Outstanding) has significantly risen to $1.08, as you can see in the graph below:

During the quarter, the company spent $150m on repurchasing 2.4m of its own shares, reducing the remaining amount authorised for repurchases to ~$1.35bn as of 30 April 2024.

5.0 Final Thoughts

Lacklustre growth, promising product pipeline.

Zoom continues to exhibit lacklustre top-line growth, as management had guided for the first half of the year (lowest revenue growth figures guided for Q2). The company continues to progress on expanding its product offering, both by the launch of new products and the addition of new features.

In my opinion, Zoom’s product development and customer care continue to be exceptional. The market will test the company’s figures during the second half of the year, when management has guided that revenue growth would reaccelerate.

Hasta pronto!

Twitter: ericsanta98

Disclosure

These are opinions only of the individual author. The contents of this piece do not contain investment advice and the information provided is for educational purposes only and no discussions constitute an offer to sell or the solicitation of an offer to buy any securities of any company. All content is purely subjective and you should do your own due diligence.Eric Santa makes no representation, warranty or undertaking, express or implied, as to the accuracy, reliability, completeness or reasonableness of the information contained in the piece. Any assumptions, opinions and estimates expressed in the piece constitute judgments of the author as of the date thereof and are subject to change without notice. Any projections contained in the Information are based on a number of assumptions as to market conditions and there can be no guarantee that any projected outcomes will be achieved. Eric Santa does not accept any liability for any direct, consequential or other loss arising from reliance on the contents of this presentation. Eric Santa is not acting as your financial, legal, accounting, tax or other adviser or in any fiduciary capacity.